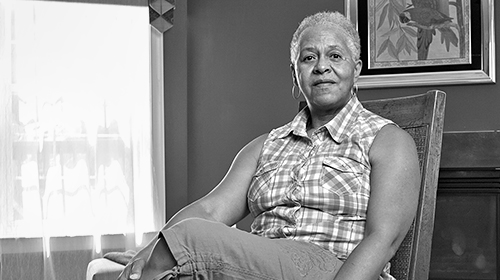

For years, Rita Winters envisioned spending her golden years of retirement at her dream house in Southern Maryland. However, as a result of events outside of Ritaãs control, her dream home placed her in a nightmare situation. Federal action is needed to stop the nightmare that Rita and millions others faced while attempting to achieve their dream of home ownership.

Rita Wintersã Story

After building equity in her home for six years, Rita decided to refinance and take out a second mortgage to cover some of her familyãs additional expenses. Unfortunately for Rita, she was caught in the same predatory lending trap that so many other people of color found themselves in over the past few years.

In predominantly Black and Latino communities, unscrupulous mortgage brokers, looking to make a profit in historically untapped and neglected markets, targeted people like Rita for risky re-finance mortgages, often with high costs and fees, and interest-only payments that ballooned after two or three years. In a rushed deal that closed in less than an hour, Rita re-financed her home, ending up with a high-cost interest-only loan that included $20,000 in origination fees and nearly doubled her monthly payment, exceeding more than half her income.

Although Rita and her family managed to cover their new exorbitantly high mortgage payments until mid-2010, their financial situation ã like that of so many families during the global recession ã deteriorated, resulting in the initiation of foreclosure proceedings. To make matters worse, Ritaãs loan, as many were at the time, was sold off by her lender as a mortgage-backed security. Since the mortgage note was now owned by a multitude of investors, it became nearly impossible for Rita to re-finance and stay in her home because of the challenges in securing approval from investors with different financial interests in the loan, .

Lasting Impact of Rampant Predatory Lending Exposed in âü¯áû颈§Ý§Ã¿« Report Justice Foreclosed

Ritaãs story is only one example of the rampant predatory lending targeted to communities of color across the country during the peak of the housing market. In Justice Foreclosed, an âü¯áû颈§Ý§Ã¿« report released last month, we examine the lasting impact that these predatory lending practices, fueled by Wall Streetãs demand for high-risk loans, have had on communities of color. Further, we recommend federal action to prevent these discriminatory practices from repeating.

The report highlights that in the five years since the housing bubble burst, lost their homes to foreclosure, with Black and Latino homeowners disproportionately impacted. This lopsided effect on communities of color around the country was driven by predatory lending, and rooted in our nationãs ongoing residential segregation and housing discrimination. The long-term harm to these communities will take years to address, because minority families hold more of their . The ripple effect of the loss of housing wealth on minority families results in a loss of inter-generational wealth, which can no longer be passed down to other generations.

Federal Action Needed

In Justice Forcelosed, we highlight key steps Congress and the Administration must take to deter financial institutions from the discriminatory and predatory practices that harmed Rita and so many others across the country. This includes increasing the civil penalties when banks and financial institutions violate the Fair Housing Act (FHA) and the Equal Credit Opportunity Act (ECOA) by engaging in discriminatory lending. Under the FHA, a violation that affects hundreds of individuals could be considered a single violation, resulting in a penalty to the financial institution of only $16,000. Putting that into perspective, the loan origination fee that the financial institution charged Rita alone was $20,000. When it only takes one origination fee to cover the cost of a penalty that resulted because hundreds of individuals were discriminated against through predatory lending, any potential deterrent effect on a financial institution to change their practices goes out the window.

Another key step is increasingfunding to the Department of Justice, so that it may adequately investigate and prosecute fair housing violations. When financial institutions know that they will be held accountable for their actions, they will be deterred from instigating discriminatory lending and create greater transparency and accountability within their own institutions. If this accountability and transparency were in place at the height of the housing bubble, Rita could have been spared the pain and loss of wealth that she faces today due to a looming foreclosure.

Action is necessary to stop the nightmare that Rita, and millions of others, faced while attempting to achieve the dream of homeownership. Additional federal policy recommendations may be found in our full report, Justice Foreclosed. The âü¯áû颈§Ý§Ã¿« continues to fight and advocate for fair housing, including, through recently filed litigation in Adkins v. Morgan Stanley and recently submitted comments to the Consumer Financial Protection Bureau.

Learn more about predatory lending: Sign up for breaking news alerts, , and .

Learn More âü¯áû颈§Ý§Ã¿« the Issues on This Page

-

Press ReleaseDec 2024

LGBTQ Rights

President Biden Must Veto Defense Bill Attacking Military Families with Transgender YouthPresident Biden Must Veto Defense Bill Attacking Military Families with Transgender Youth

WASHINGTON ã The U.S. Senate today passed a version of the National Defense Authorization Act that would ban coverage for gender-affirming care for transgender youth whose parents are active-duty military personnel. The âü¯áû颈§Ý§Ã¿« is opposing final passage of the defense bill over the inclusion of this health care ban and calling on President Joe Biden to veto the bill. Section 708 of the NDAA would prohibit insurance coverage for ãmedical interventions for the treatment of gender dysphoriaã such as hormone therapy and puberty-suppressant medications, which Speaker Mike Johnson says would ãpermanently ban transgender medical treatment for minors.ã The same treatments would be covered by TRICARE for any medical purpose other than treating gender dysphoria, the clinical diagnosis for the psychological distress experienced by transgender people related to their gender identity. ãBy passing this bill, the House and Senate are forcing thousands of active-duty service members to choose between their careers in the military and the future of their transgender children,ã said Mike Zamore, national director of policy & government affairs at the âü¯áû颈§Ý§Ã¿«. ãThis unconscionable and unjustifiable attack on those families stands in direct contrast to President Joe Bidenãs legacy of defending the civil rights of transgender Americans ã including when few in his own party showed the courage to do so. President Biden should cement his legacy by vetoing this bill and sending it back to Congress to pass without Speaker Johnsonãs last minute health care ban for servicemembersã kids.ã If signed by President Biden, this health care ban would be the first new anti-LGBTQ provision enacted by Congress and signed into law by the president since the enactment of the militaryãs since-repealed ãDonãt Ask, Donãt Tellã policy for LGBTQ servicemembers and the since-repealed federal law barring recognition of same-sex marriages known as the Defense of Marriage Act. It is unknown how many transgender youth are currently enrolled in TRICARE or how many of those enrolled are currently receiving coverage for gender-affirming care. In one 2022 analysis, 2,500 minor patients sought care for gender dysphoria through TRICARE Prime insurance at military or civilian treatment facilities in 2017, and 900 received puberty suppressants or gender-affirming hormones. Earlier this month, the Supreme Court heard oral arguments in a landmark case brought by the âü¯áû颈§Ý§Ã¿«, the âü¯áû颈§Ý§Ã¿« of Tennessee, Lambda Legal, and Akin Gump on behalf of three families and a medical provider challenging a Tennessee ban on gender-affirming hormonal therapies for transgender youth on the grounds the ban violates the Equal Protection Clause of the U.S. Constitution. -

Press ReleaseDec 2024

LGBTQ Rights

Montana Court Blocks State From Refusing to Correct Sex Markers on Transgender People's Birth Certificates and Driver's LicensesMontana Court Blocks State From Refusing to Correct Sex Markers on Transgender People's Birth Certificates and Driver's Licenses

HELENA, Mont. ã A Montana court has granted a preliminary injunction preventing the state of Montana from enforcing policies that bar transgender people from obtaining accurate sex designations on their birth certificates and driverãs licenses. After a prior restriction on amendments of birth certificates was struck down by the courts, in early 2024 the state of Montana enacted a new rule that categorically bars transgender Montanans from correcting the sex designation on their birth certificates. Around the same time, the Montana Department of Justice adopted a policy similarly restricting amendment of driverãs licenses. The plaintiffs challenged these policies in state district court, arguing that they violate various constitutional provisions, including the right to equal protection of the law. In a recent Montana Supreme Court decision, two justices concluded that discrimination on the basis of transgender status ã as the state is engaging in here ã is a form of sex discrimination that violates the Montana Constitutionãs equal protection clause. The plaintiffs, two transgender women, are represented by the âü¯áû颈§Ý§Ã¿«, the âü¯áû颈§Ý§Ã¿« of Montana, and Nixon Peabody LLP. Plaintiff Jessica Kalarchik, a veteran who served in the United States Army for 31 years, said: ãAfter finally being able to live my life openly as the woman I know myself to be, I am frustrated that my birth state, Montana, wants me to carry around a birth certificate that incorrectly lists my sex as male. I live my life openly as a woman, I am treated as a woman in my daily life, and there is no reason I should be forced to carry a birth certificate that incorrectly identifies me as male. Fortunately, the court agrees that this ridiculous policy should not be in effect.ã ãOnce again the State of Montana chose to adopt a draconian policy that is clearly intended to marginalize transgender Montanans, only for that discriminatory action to be blocked by the courts,ã said Akilah Deernose, executive director for the âü¯áû颈§Ý§Ã¿« of Montana. ãHere in Montana we treasure our right to privacy and to live our lives free from governmental intrusion. The State of Montana clearly has not learned any lessons from the past few years, where courts have repeatedly struck down unconstitutional laws targeting transgender Montanans.ã ãForcing anyone to carry documents that contradict their identity unjustly violates their rights to privacy, equal treatment, and not being compelled to convey a government message about their sex that they disagree with,ã said Malita Picasso, staff attorney for the âü¯áû颈§Ý§Ã¿«ãs LGBTQ & HIV Project. ãSuch a policy marks transgender people for further mistreatment and discrimination, essentially requiring them to carry papers that out them as transgender any time they need to provide identity documents. Fortunately, the court has refused to allow the state of Montana to subvert the freedom of transgender Montanans to control their own identity as this case goes forward.ã In granting the plaintiffsã motion for a preliminary injunction, the court held, ã[i]f the challenged state actions discriminate against transgender individuals on the basis of their transgender status, they also necessarily discriminate the basis of sex.ã The state has the option of appealing the district courtãs ruling to the Montana Supreme Court, but the underlying case will proceed in district court. A trial has not yet been scheduled. -

FloridaDec 2024

LGBTQ Rights

Keohane v. DixonKeohane v. Dixon

On September 30, 2024, the Florida Department of Corrections rescinded its policy regarding treatment of gender dysphoria, which allowed for hormone therapy when deemed medically necessary, as well as access to clothing and grooming standards that accord with oneãs gender identity. Under this new policy, grooming and clothing accommodations have been stripped away, and hormone therapy is not permitted unless an exception is deemed constitutionally required. The âü¯áû颈§Ý§Ã¿« brought a class action challenging the policy. -

IdahoDec 2024

LGBTQ Rights

Robinson v. LabradorRobinson v. Labrador

Two incarcerated transgender women have sued the state of Idaho alleging that HB 688, a 2024 law barring state funding for gender-affirming medical care for transgender people, denies them access to the health care their doctors have prescribed for them and is a violation of their Eighth Amendment right to be free from cruel and unusual punishment. They represent a class of all incarcerated folks within the state of Idaho who face the loss of hormone therapy due to HB 668.